A funny story: last weekend I was packing up furniture from my parents’ garage to move into a rental house and was stopped by a passerby who asked “are you packing up for college?”. My parents thought it was hilarious (it also made them about 20 years younger, which I'm sure they liked). I corrected her, but when I’m 60 and mistaken for 40 I may just let it slide.

In case you were also thinking I appear young, I just celebrated my 38th birthday and 13th wedding anniversary this week, have two kids and 14 years’ experience as a financial advisor. And since my husband and I just purchased a rental property, today we're going to focus on homeowner's insurance since it's fresh on my mind.

What is homeowner’s insurance?

Homeowners insurance is a surprisingly consistent policy across insurers that cover losses to a dwelling. There are 4 types that cover owned homes: HO-1, HO-3, HO-2, and HO-8. Of these, HO-3 is by far the most common type and in addition to covering the structure of a home, also covers “named peril” coverage for personal property like furniture and clothing.

There are two other common policies: HO-6, which is a condo policy and covers everything inside the sheet rock, and HO-4, a renter’s policy, which covers only the renter’s personal belongings.

It’s worth reading your homeowner’s policy someday as it does protect what’s oftentimes your most valuable asset second only to your practice, and probably your most meaningful.

What isn’t covered?

With homeowner’s insurance it’s important to take a step back and look at how insurance works. Insurance exists when there’s a pool of risks that aren’t related. Based on that pool, insurers can determine their average loss rate, and everyone’s premiums combined cover those losses.

The reason this is so important is that without a special policy, insurance policies don’t cover things that would affect your whole neighborhood—earthquakes, hurricanes, acts of war. Some policies cost an arm and a leg through insurance companies (if you’ve tried to insure a beach home in Florida recently you’ll know this), and others are inexpensive (fun fact: an earthquake policy in Atlanta costs less than $20/month), and others are so impossible to cover they are actually managed by the federal government (flood zone policies).

Common Homeowner’s Insurance Pitfalls

Homeowner’s insurance is a common area to find cost savings. Insurance companies tend to stamp a standard increase in the cost to rebuild a home, and over time it can grow beyond what’s reasonable. For example, I’ve seen a home worth $450,000 be insured for over $700,000—and insurance doesn’t include the cost for the land. Take a peek at your insured value annually to make sure it seems reasonable with your local cost to build.

One of the most common insurance claims in a home is a basic one: water. The toilet overflows, a pipe bursts, a leaky roof… I’m seen policies that only cover a set dollar amount, like $5,000. If a toilet leaks upstairs onto your hardwoods then seems through the ceilings downstairs you are most assuredly looking at more than $5,000 of damage. I prefer to see this as a % of the dwelling.

Along these lines, water back up is generally NOT covered under a standard policy and should be added. Last, if said water damage caused mold that needed remediation, it’s important to make sure your policy covers that as well.

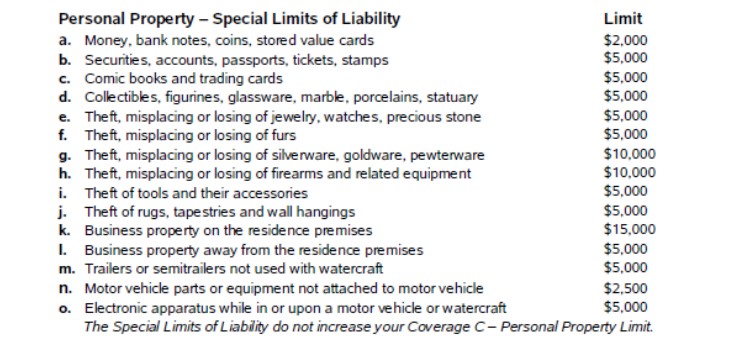

The last common issue I see is the limits on personal property coverage. At a glance this coverage can seem great—hundreds of thousands of dollars for the contents of your home! However, when you read into policy documents, the actual coverage for specific items can be less than appealing, the most notable for most couples being the limit on jewelry. See an example set of policy limits below. If you have a collection, artwork or jewelry worth more than these limits, you should consider buying a special policy to cover these items.