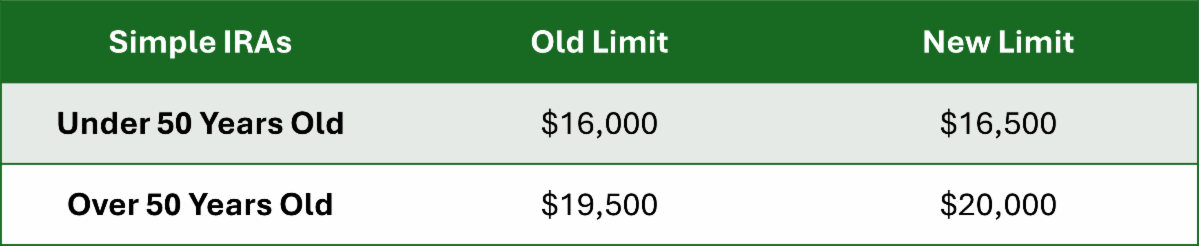

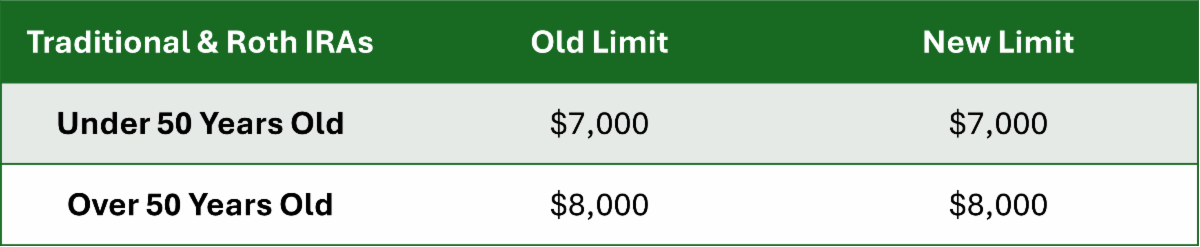

Traditional and Roth IRAs

There can be some confusion about the role of traditional and Roth IRAs so it’s worth recapping a bit. A traditional (or rollover) IRA is tax deferred, meaning that usually money goes in pre-tax, creating a credit on a tax return, then is taxed like a paycheck when it comes out. Contributions that cannot be deducted are called "non deductible" contributions (explained below) and those are supposed come out tax free (note that it’s your responsibility to keep up with those which can be challenging over the years).

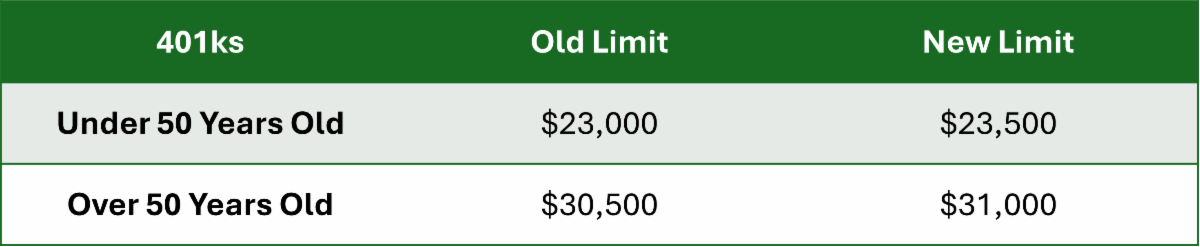

When are IRA contributions non-deductible? First, if you or your spouse participate and any kind of employer sponsored plan (401k, Simple, SEP, etc) it impedes your ability to deduct traditional IRA contributions. In some cases, spouses can take the deduction if household income is less than $126,000 (2025) and single tax payers can take a deduction if incomes are less than $79,000 (2025) with some phase out levels.

Not done correctly non-deductible contributions to a traditional IRA are not good—you’re essentially taking money you’ve already paid taxes on and having it taxed again when you withdraw it.

A Roth, however, is funded with after-tax money that grows tax free forever. Roths are a great vehicle and I like to see everyone who can participate do so. To directly contribute to a Roth for 2025 your adjusted gross income (line 11 on your tax return) must be less than $236,000 for married filing jointly and $150,000 for single filers with some phase out levels. However, it is possible for some doctors to do what's called a backdoor Roth if you have no other pre-tax IRA money. Married filing separately tax payers cannot contribute directly to a Roth.

Roth versus traditional questions usually boil down to income, and as you might imagine many taxpayers don’t know where they fall in their AGI until tax time. Consequently, the deadline to contribute to these vehicles is April 15th of the following year. |