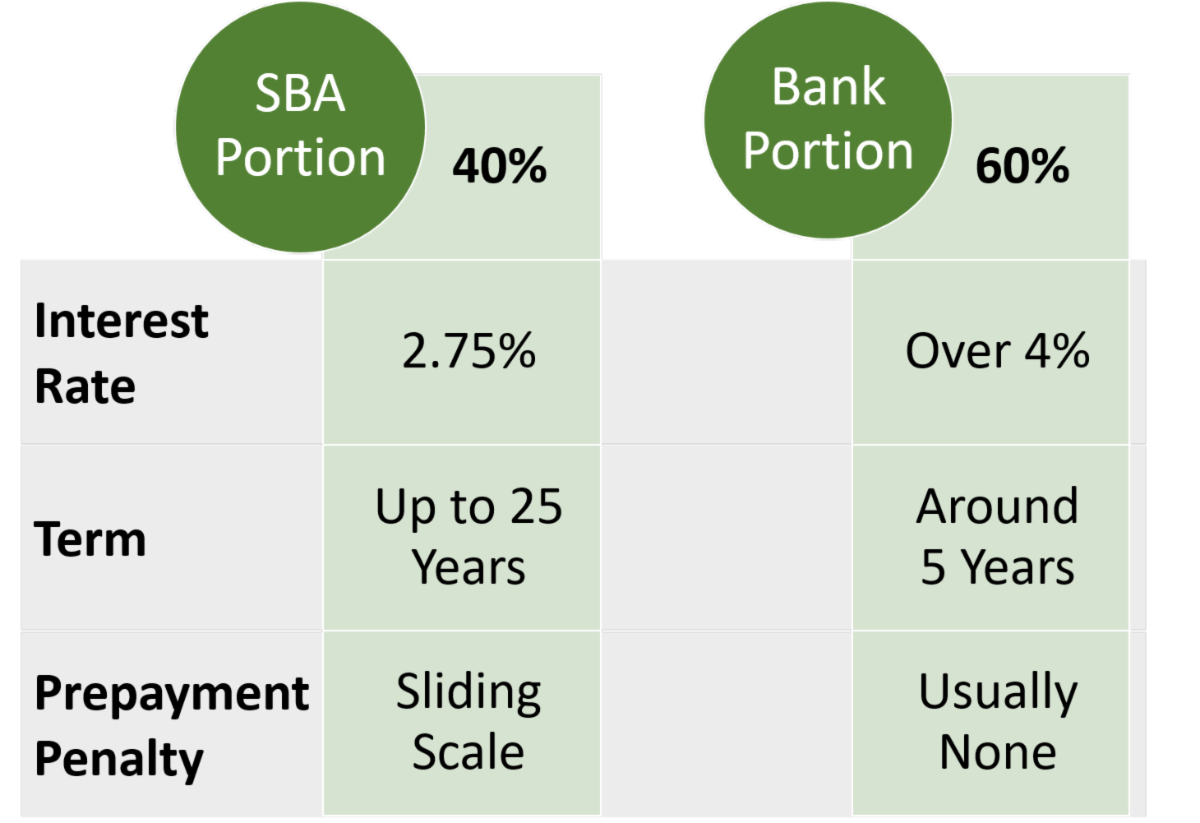

Of course my next question to Stephanie was why wouldn’t a doctor with a lower loan to value refinance at the 90% loan-to-value, then immediately pay off higher interest rate bank portion with the amount they were able to pull out with the refinance. The answer: closing costs. The average 504 loan has closing costs of 2-2.5%, which is a lot of money to pay to upfront just turn around and pay off a loan.

So who does the 504 loan/refinance work for? Stephanie says this is a great deal for a practice owner buying new real estate, but for refinances the difference in the combined interest rate needs to be greater than 1%. She also reminded me that historically speaking, the 4-5% rate the bank portion is offering is still a good rate.

One other caveat: 504 real estate needs to be at least 51% owner occupied (used by the practice or other businesses the OD owns) to count, otherwise it must qualify based on rental income from existing leases. It's also important to note that most SBA loans require a second lien on your home, something that surprises a lot of borrowers.

In summary, for doctors purchasing new practice real estate, the SBA 504 can be a great deal for an attractive long term loan and reasonable intermediate bank loan. For refinances, a loan's current interest rate really needs to be around 5% or higher to justify the cost, or can make sense if a doctor has a compelling reason to refinance just to extend out amortization and increase cash flow.

If you have questions about the 504 program, feel free to reply back with your situation, or even better, Stephanie graciously offered to share her contact information—she’s the expert!

StephanieBrown

SVP Commercial Banker

3333 Riverwood Parkway, Suite 300, Atlanta, GA 30339

O: 678-449-3531 | M:404-414-4211

NMLS# 1213697

Have a great week,

Natalie