{DISCLAIMER: I always hesitate to write something like this because it is absolutely not political commentary; it’s simply education on why the news, economy and stock market are acting the way they are. Please read it as such and I promise my next article will not mention the White House!} Greetings! Over the last month (and this week in particular) you may have noticed President Trump isn’t too keen on some of the economic policy keyholders in the US right now, in particular the Federal Reserve. First, he allegedly called the chairman Jerome Powell a stubborn moron and in a recent meeting dug in deep on the fact that the Federal Reserve is over budget on renovations planned in 2017 and being executed today, culminating in a very awkward visit last week. I someone doubt someone who operates a real estate empire is truly surprised at how cost overruns on a project planned pre-covid and executed post-covid, so where’s the rub? First, a little backdrop. The Federal Reserve has two primary roles: - To create a stable price environment (aka inflation) and maximize sustainable employment levels

- To supervise and regulate banks for the safety and soundness of US financial systems. Banks are always a concern post 2008 and even more recently with the fall of Silicone Valley Bank in 2023 but the more recent and painful sting for all Americans has been inflation post-covid, peaking at 9.1% in June of 2022- levels we haven’t seen since the 1970s. In this writer’s opinion what the Federal Reserve has pulled off what I frankly thought was impossible: in a matter of a few years pulling inflation down to hovering at the 3% mark (year over year) without tanking the stock market or the economy.

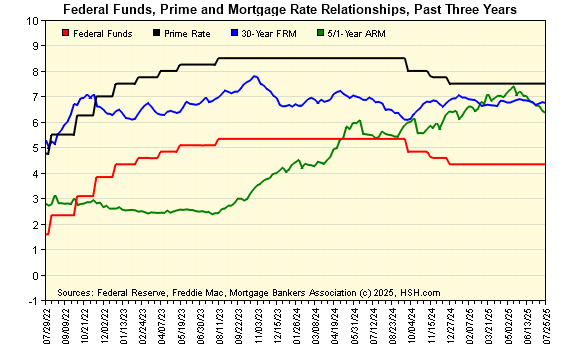

So what’s President Trump’s problem with the Federal Reserve? Well, the political dynamics today are a weird, tangled web. Government debt has ballooned post covid and interest rates are continually putting pressure on the economy. Current administration's proposed fixes included revamping the tax bill (which while the numbers look big on paper it’s a drop in the bucket on what an actual debt fix looks like), eliminating drains on the economy like illegal immigration and inefficient government operations and imposing tariffs on other countries to raise funds for the government and try to drive inputs and production back to the US. The state of US debt is a real long-term problem. While it’s still one of if not the safest investment in the world, it was downgraded on the debt scale earlier this year because there will be issues in the future if something doesn’t give. So what would help? In theory, lower interest rates. Guess who doesn’t use government debt load as part of their rate adjustment considerations? The Federal Reserve. And the abruptly fired head of the Bureau of Labor Statistics after jobs and payrolls were adjusted by the largest level since the 1970s? There is a lot of speculation this is over mismatched agendas. Who’s right? I really don’t know, and I’m not sure anyone does. Managing the economy doesn’t come with a hard and fast rule book on what works and what doesn’t, especially during times like global pandemics and the years following. In the Federal Reserve’s defense, they enjoy pretty much complete autonomy from the White House to prevent government interference in it’s mandate to keep the economy stable. My family recently went to Argentina where they’ve had wild swings in monetary policy based who was in office. Inflation was 211% in 2023 (per the IMF), estimated at almost 250% in 2024 and expected to reel back to around 36% in 2025. Could you imagine having $1mm in 2023 in the bank and it being less than $500,000 in one year? There are very, very valid reasons for separate of monetary policy and elected officials. So Trump would like rates to come down to help ease the burden of US debt and also because let’s face it: buying a house, a business, real estate…. It’s all a lot more expensive than we’re used to (although still pretty low historically speaking). And the Federal Reserve… well, their inflation target is 2% (remember we’re tottering around 3%) so there’s still have a ways to go before they want to start lowering. Tariffs in particular are a point of contention because at it's core, a 15% or 25% or 55% increase in the cost of a cost or the input into a good is in fact inflation. You can be assured the Federal Reserve has a hawk eye on the impact, most of which just went back into action this past week after a pause for negotiations. The greatest irony is that the Fed reducing rates doesn’t really impact everything I just outlined as important. Their rate is the overnight lending rate to banks, which impacts floating rate debt (think a HELOC or credit card) immediately but not necessarily longer term debt like a practice purchase loan, car loan or mortgage, which are based on investor expectations of what rates will do in the future, NOT what the Federal Reserve does. The below graph is the perfect illustration of how the Federal Reserve rates change actions do not always equal a change in longer term debt rates. Line color explanation below. - Federal Funds (in red) is the rate the Federal Reserve determines - Prime Rate (in black( is a rate banks regularly price off of to consumers and businesses - The 30-year FRM (blue line) is the average 30-year mortgage rate - The 5/1 ARM (in green) is an average five year mortgage rate |