Last Monday marked the deadline to get in your tax returns or extensions in, making Tuesday most CPA’s favorite day of the year. Since taxes are fresh on most practice owners' minds, this seems like a good time to bring up the top tax mistakes I see as you look forward into the rest of 2022.

Mistake #1- Buying equipment/spending money to avoid taxes

I do understand it’s painful to stroke a large check to Uncle Sam, but the saying about death and taxes exists for a reason. Purchasing equipment or incurring other non-necessary expenses is a common tool I see ODs use to mitigate their tax bill. When new equipment is needed or helps a practice grow revenues, this makes a lot of sense. But buying just for the sake of avoiding a tax bill is missing the forest for the trees.

Even in the top federal tax bracket (currently 37%), for every dollar spent buyers are saving 37₡ but spending 63₡ to do so. Imagine a practice incurred an unnecessary $50,000 of deductible expenses every year for 10 years to mitigate their tax bill. That’s $315,000 that could have been invested for retirement in order to save $185,000 in taxes, which will inevitably be recaptured when a practice is eventually sold (usually in a higher tax bracket year than the current one).

Mistake #2- Using bonus depreciation to completely eliminate a tax bill

In 2017, the Tax Cuts and Jobs Act allowed businesses to deduct “bonus depreciation” and within limits take 100% of depreciation in that calendar year. I see this a lot with equipment and build out costs, but very rarely does it make sense to take all the depreciation in one year. While it is certainly nice to have a year with no tax liability (and is much easier for CPAs to calculate and track), the nature of the progressive tax system means this approach rarely makes sense.

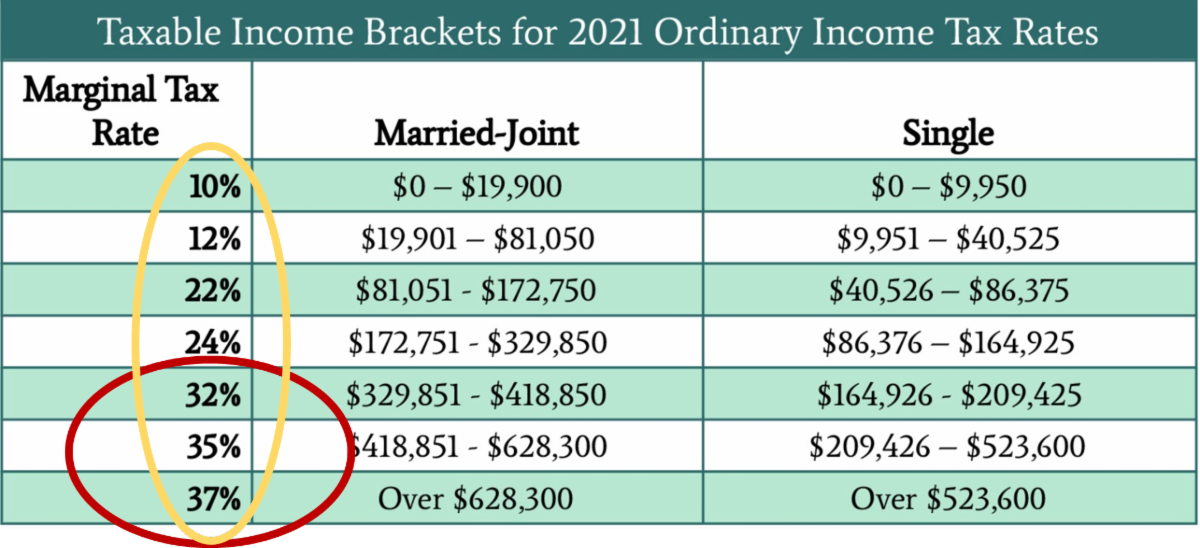

When a tax liability is reduced to $0 in a given year, it is taking tax dollars out of the 10%, 12%, 22%, 24% etc tax bracket (see gold circle). But when depreciation is spread over a normal schedule, the dollars being deducted against are in the tax payer's highest bracket (see the red circle).

There are some situations where bonus depreciation makes lots of sense, like using the opportunity to convert pre-tax IRA money to a Roth or in a sale year. But more often than not, it’s better to spread depreciation out over a number of years.