Greetings and happy Sunday!

With mortgage rates dropping, I’m getting asked regularly if now is a good time to refinance. The answer is usually “it depends”. It’s very easy to get caught up in the appeal of reduced monthly payments, but it’s not always the best financial decision. Wondering why? It boils down to two main factors: closing costs and loan amortization schedules.

You probably didn't memorize all the line items at your last mortgage closing, but typically between attorney fees, appraisals, origination fees (which allow you to “buy down” the interest rate by paying points, which is essentially interest in advance), recording fees, title fees, etc. The average closing costs average between 2% to 6% of the loan balance. So on a $500,000 loan, closing costs would fall between $10,000 and $30,000. Usually this is wrapped into the loan balance so you don’t come out of pocket but it is still a very real cost.

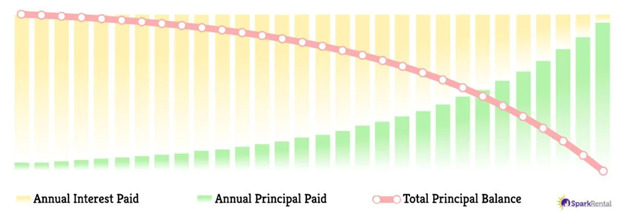

The second sneaky thing about a refinance is that it resets the amortization schedule. With loan amortization the beginning of the loan is mostly interest and by the time it’s almost paid off it’s mostly principal. On a 30-year loan a whopping 83% of the first payment is interest, and after 5 years borrowers will have paid 70% of the interest on the total loan amount. So refinancing resets that interest/principal mix. See illustration below: |